Let me ask you something personal. Not about money. Not about insurance. Just a simple question:

“If you needed help — real help, day-to-day care — would you want your kids dropping everything to provide it?”

Almost everyone answers the same way: No. Absolutely not. That is the last thing I would want.

And yet, most people have done nothing to prevent exactly that from happening.

That’s the conversation we want to have with you today. Not the one about statistics or premium rates or actuarial tables. The one about why we don’t plan for something we already know is coming.

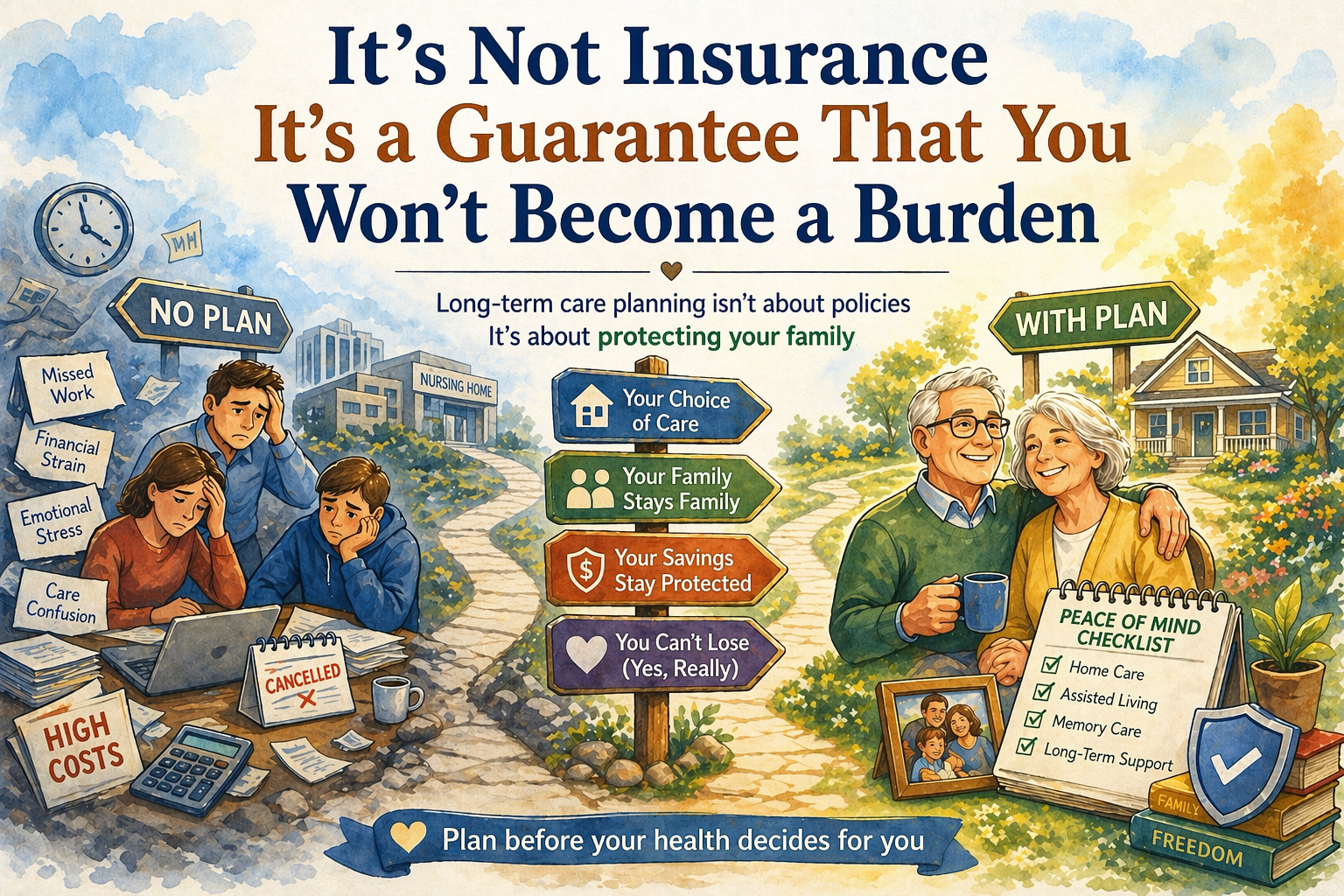

The Word “Insurance” Is Ruining the Conversation

Here’s something to consider: if long-term care planning were called anything other than insurance, everyone would want it.

Call it a Care Fund. A Longevity Guarantee. A Family Protection Account. Whatever you like — the moment people understand what it actually does, they’re in. The resistance isn’t to the concept. The resistance is to the word.

Insurance, as a category, carries baggage. We pay for car insurance and hope we never use it. We buy homeowner’s insurance and quietly resent the premium every year when the house doesn’t burn down. Insurance, in our minds, is a bet against ourselves. We pay in. We hope we lose.

Long-term care planning is fundamentally different — and I mean that in a structural, contractual, guaranteed way — but because it wears the same label, people tune it out before the conversation even starts.

The obstacle isn’t logic. It’s psychology.

Here’s the Reality Nobody Wants to Sit With

Almost nobody dies suddenly anymore. Modern medicine has gotten remarkably good at keeping us alive. What it hasn’t solved is what happens in the years — sometimes many years — before the end. Strokes leave people needing daily assistance. Dementia progresses slowly, and the person you love is still there but unable to manage alone. Falls, surgeries, chronic illness — they create care needs that don’t resolve in a few weeks.

Most of us will go through a period where we need meaningful help. It won’t be brief. And it won’t be free.

The question isn’t really IF you’ll need care. The question is who’s going to provide it — and what it’s going to cost them.

What “Family Handles It” Actually Looks Like

When there’s no plan, families step in. That sounds loving, because it is. But let’s be honest about what it means in practice.

It usually means a daughter — statistically it’s almost always a daughter — reducing her hours at work, or leaving her job entirely. It means her retirement savings slow down or stop. It means her marriage is under strain. It means her kids watch her sacrifice and wonder, quietly, if this is what’s coming for them too.

It means your son, who has his own family and his own demands, is suddenly navigating care facilities, insurance calls, and medication schedules between work meetings. It means family gatherings start to carry weight they were never supposed to carry.

None of this happens because anyone failed. It happens because there was no plan.

“I don’t want to be a burden” is the most common thing I hear. But it only matters if you act on it before it’s too late.”

So Why Don’t People Plan?

We’ve had hundreds of these conversations. The resistance almost always comes down to one of three things:

First, denial. It’s genuinely hard to picture yourself needing help getting dressed or remembering your grandchildren’s names. The future version of you who needs care doesn’t feel real yet. Planning for that person requires imagining something most of us actively avoid.

Second, avoidance. Dealing with insurance feels like a chore. It’s complicated. It requires paperwork, medical questions, and decisions you’d rather not make today. The path of least resistance is to put it off — and then put it off again.

Third, and this one is quieter: we associate needing care with the end of life, and we don’t want to go there mentally. Planning for long-term care feels like planning for decline, and nobody wants to spend an afternoon doing that.

But here’s what we want you to consider: the planning doesn’t make the decline more likely. It just means that if it happens, it doesn’t also become a financial and emotional catastrophe for everyone you love.

What the Planning Actually Does

When someone has a proper long-term care strategy in place, here’s what changes:

You get to choose where you receive care. Your home. A facility you actually like. Not whatever Medicaid will cover. That choice — and the dignity it represents — is what the planning buys.

Your children get to be your children, not your case managers. They show up because they love you, not because they have no other option.

Your savings stay intact. A serious care event without coverage can deplete a lifetime of savings in two or three years. With a plan, that doesn’t happen.

And here’s the part people don’t expect: with the right structure, you can’t lose. If you need care, the policy pays out. If you never need care, there’s a death benefit for your heirs. If you change your mind, you can walk away with your money back. Those are the three possible futures — and all three of them work out.

“You can’t lose” is not a sales pitch. With the right plan, it is literally the contract.

The One Catch

There is one thing that can take this option off the table permanently: your health.

Long-term care planning requires medical underwriting. If you’re healthy today, you qualify. If you wait until a diagnosis comes — and they always come eventually — the window closes. Not narrows. Closes.

This is the part I want you to take seriously. Not because we’re trying to create urgency artificially. But because I’ve had to have the harder conversation too many times — the one where someone calls me six months after they should have, and the opportunity is gone.

This Isn’t a Hard Conversation. It’s a 30-Minute One.

If anything here resonated — if you thought of a parent, or yourself, or a spouse — that’s the signal. Not to panic. Just to take the next step.

A conversation with us costs nothing. We ‘ll show you exactly what your exposure looks like in real numbers, and what a strategy would cost to fix it. No pressure. No commitment.

The only regret we ever hear in this business is from people who waited too long. You don’t have to be one of them.