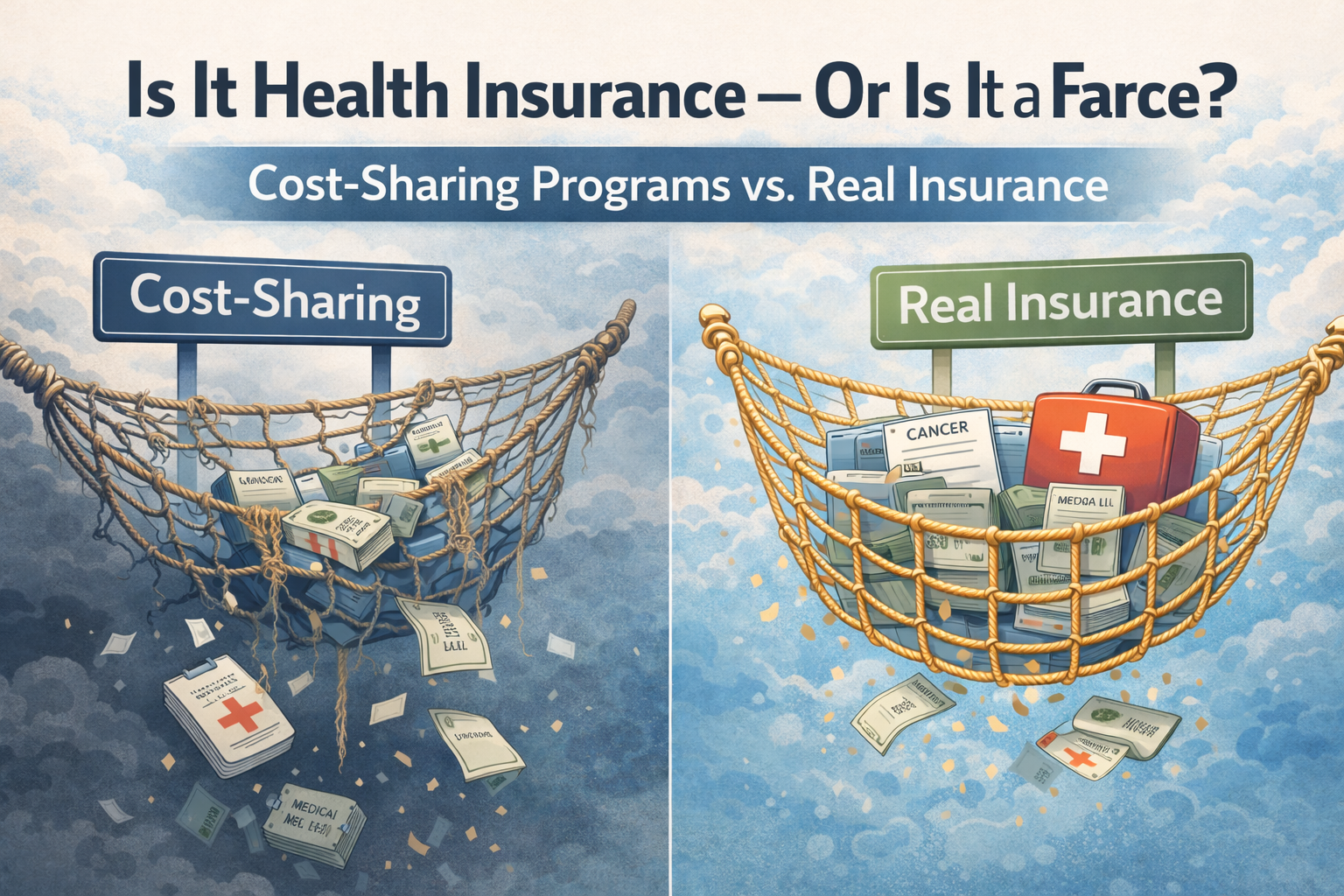

Cost-Sharing Programs vs. Real Insurance

As Affordable Care Act subsidies expire and premiums jump for millions of Americans, the health insurance marketplace is quietly shifting in a dangerous direction.

People aren’t just shopping for better plans.

Many are abandoning real insurance altogether.

Faced with dramatic premium increases, families are turning to “alternatives” like Medi-Share, Christian Health Ministries, and other medical cost-sharing programs. These options are marketed as affordable, community-based solutions that look and feel like insurance.

But they are not insurance.

And in many cases, they do not protect families when it matters most.

The Illusion of Coverage

Cost-sharing programs operate outside state insurance regulation. They are not legally required to pay claims, cap out-of-pocket costs, or guarantee coverage for serious illness.

They can:

- Decline claims

- Limit reimbursements

- Change rules mid-stream

- Set internal caps without regulatory oversight

When care is routine, the system may appear to work.

But healthcare is not routine.

When someone faces cancer, transplants, neonatal care, or trauma — claims in the hundreds of thousands or millions — there is no insurance company standing behind that promise. There is only a pool of other participants and a committee deciding what they are willing to share.

That is not protection.

That is hope.

The Real Financial Risk

The danger isn’t medical access. It’s financial collapse.

When catastrophic illness meets inadequate coverage:

- Savings disappear

- Retirement accounts are liquidated

- Home equity is tapped

- Homes are sold

- Long-term security is permanently damaged

Not because care was unavailable.

But because people believed they were insured — when they were not.

This is how decades of financial stability can vanish with a single diagnosis.

Why This Is Happening Now

Enhanced ACA subsidies temporarily hid the true cost of health insurance. For several years, many middle-income families paid artificially low premiums.

Now those subsidies are expiring.

Premiums are resetting to real prices.

And millions are experiencing shock.

The system did not prepare consumers for this transition. So they do what people always do when prices rise — they look for cheaper substitutes.

Even if the substitute does not truly work.

The Negotiation Myth

Cost-sharing programs often claim they “negotiate” medical bills like insurers.

They do not.

Insurance carriers have contracted networks, negotiated rates, legal standing, and regulatory oversight. Cost-sharing programs rely largely on provider goodwill, cash discounts, and informal negotiations.

In major hospital systems, that difference is not small.

It is the difference between protection and exposure.

A System Under Strain

As more healthy people exit real insurance, risk pools weaken. Premiums rise further. More people leave.

This cycle threatens the stability of the entire market.

At the same time, more families are walking into catastrophic financial risk without realizing it.

Final Thought

Health insurance exists for one reason:

To protect families from financial disaster when health fails.

When programs offer the illusion of protection instead of real protection, the consequences are not theoretical – people find a way to pay for everything that is important for them and this is unfortunately something we will all have to continue to navigate and manage until a better alternative comes along.